Wicked Problem CashCritter

TEAM MEMBER

Alondra Alvarez

Jim Gaile

Pui Ki (Peggy) Chan

Ella Timmons

Wicked Problem

People don’t understand their finances. We have financial (il)literacy.

Financial Literacy:

There is a lack of understanding of the basic home economics, wealth management, long-term debt.

balancing a bank account

understanding actual home economics

credit score math

buying a home for the first time

Understanding how credit cards work

(quiz feature daily)Home Economics is no longer taught in school, this might help rectify.

Research:

Learn more about age correlation to specific financial topics.

Understand what certain age segments are suffering from in terms of finances.

Investigate current resources that are available.

What do they not have access to?

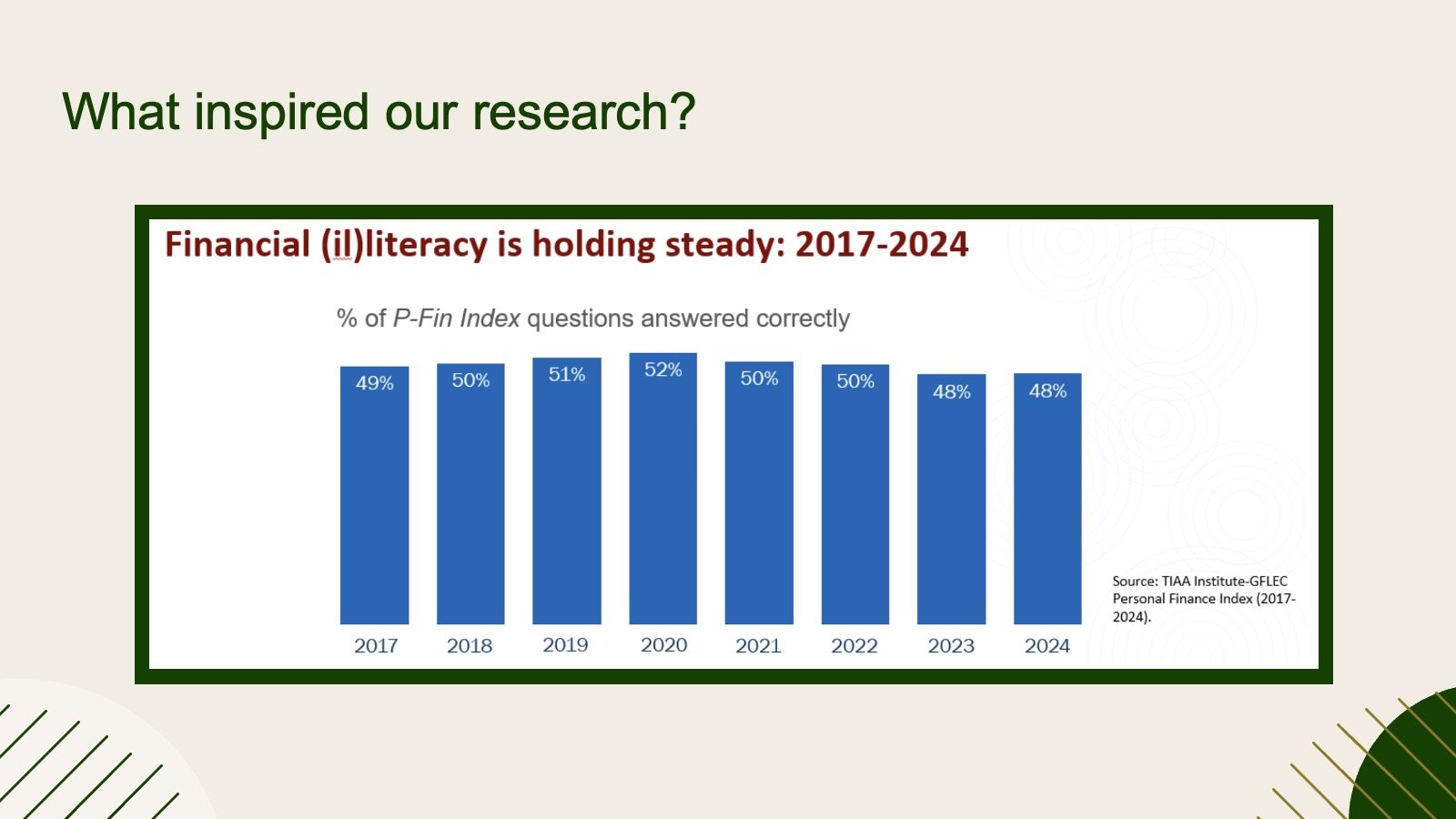

The number of people in the US who understand basic financial principles has not significantly changed for eight consecutive years.

One in-depth barometer of personal finance knowledge is 28 questions given annually to US adults, known as the P-Fin Index. The index explores eight functional areas across finance, such as earnings, savings, insuring and comprehending risk.

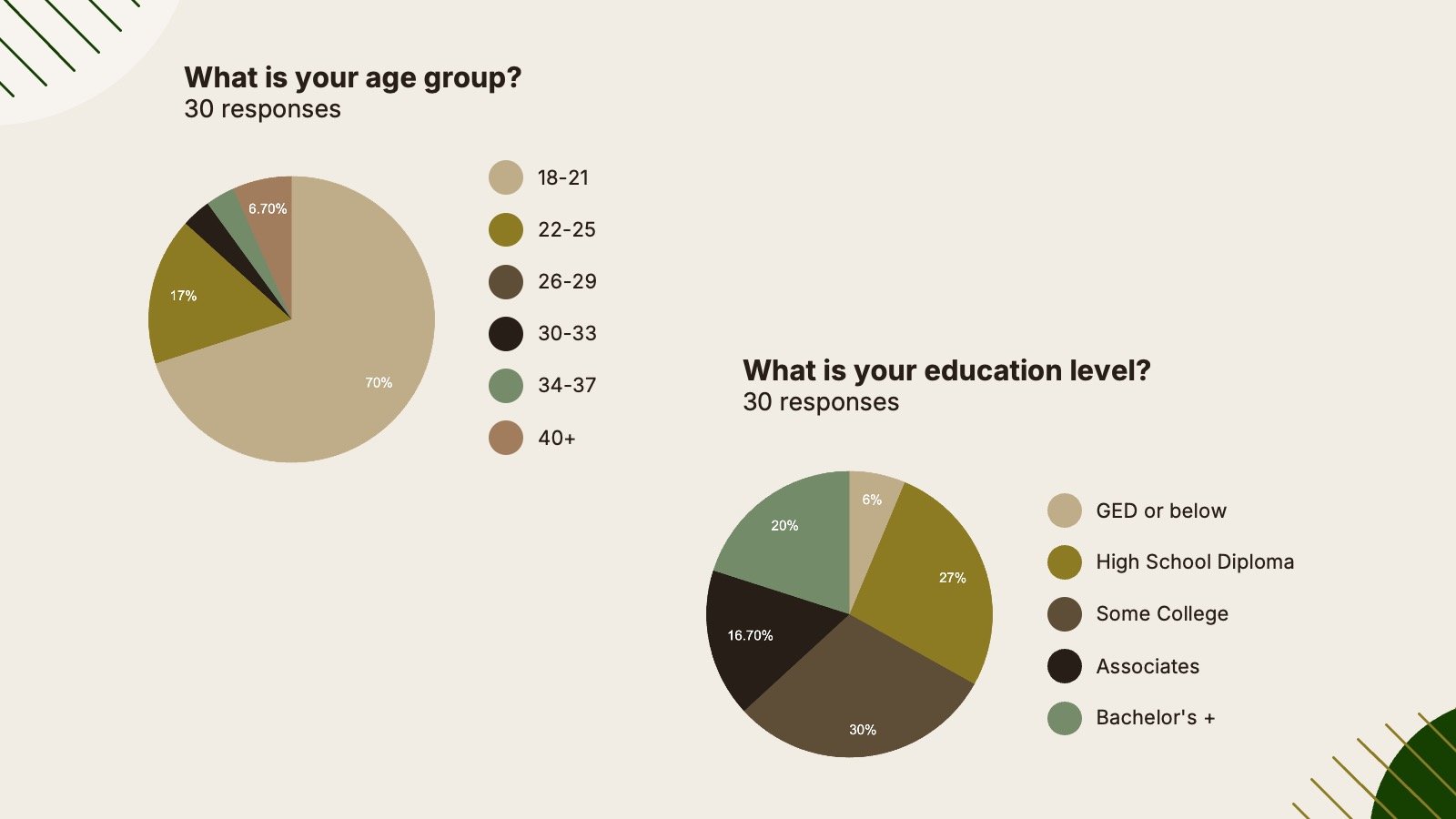

Relevant: our current generation, gen z is the generation scoring the lowest scores

Missouri was the first state requiring personal finance courses in high school in 2000 and California is the 26th and most recent state to pass legislation requiring high schoolers to take a personal finance course

The significantly low results of personal finance across generations made us question the effectiveness of the curriculum and the manner in which this information was presented to students + the lack of retention should be studied for the sake of providing resources and methods that allow students to not only learn about personal finance but retain that information in order to apply it later on in life.

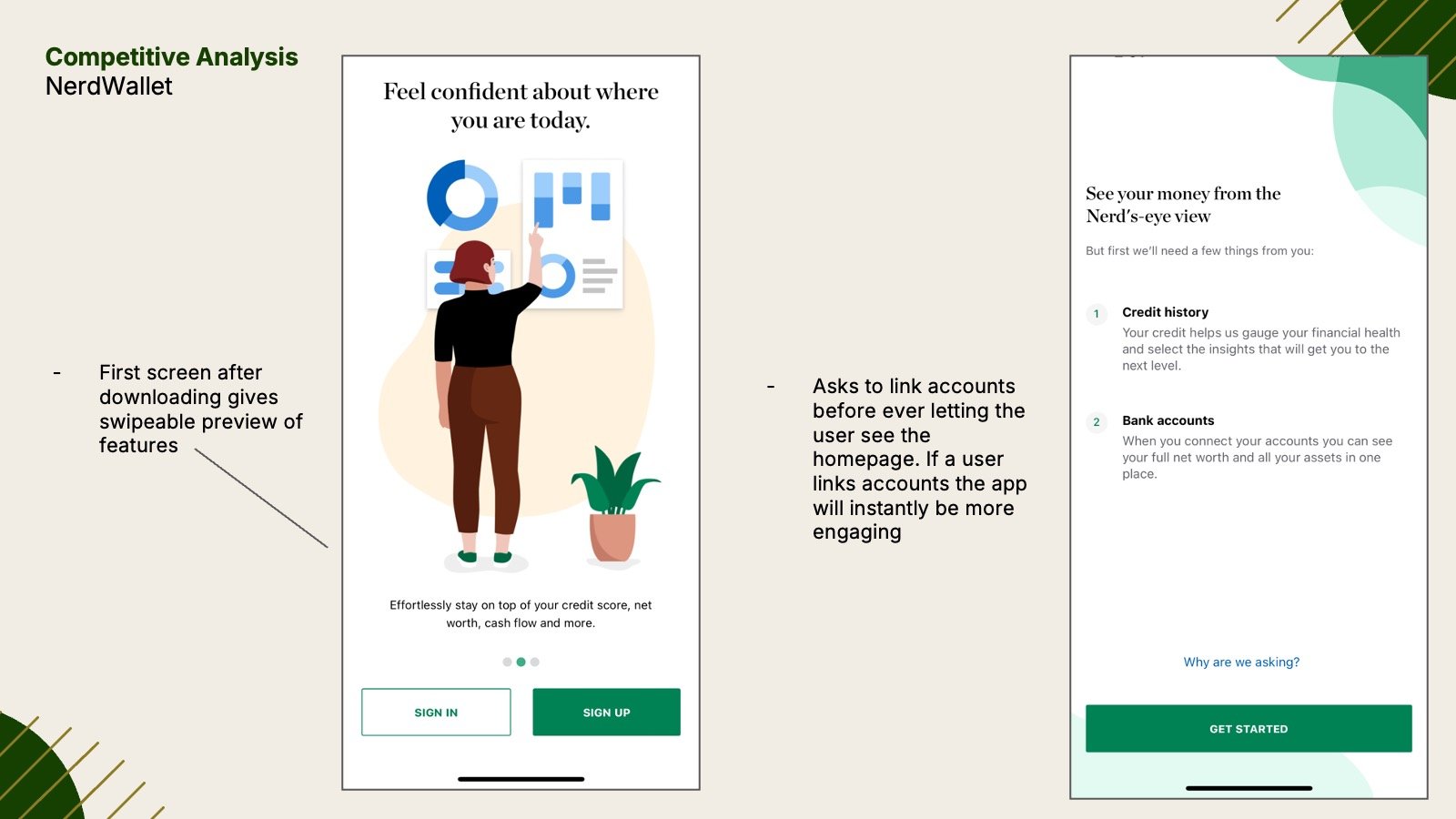

EXTRA

A 2014 study published by the Federal Reserve found students who had a financial education requirement had higher relative credit scores and lower relative delinquency rates than those in states without such a requirement.

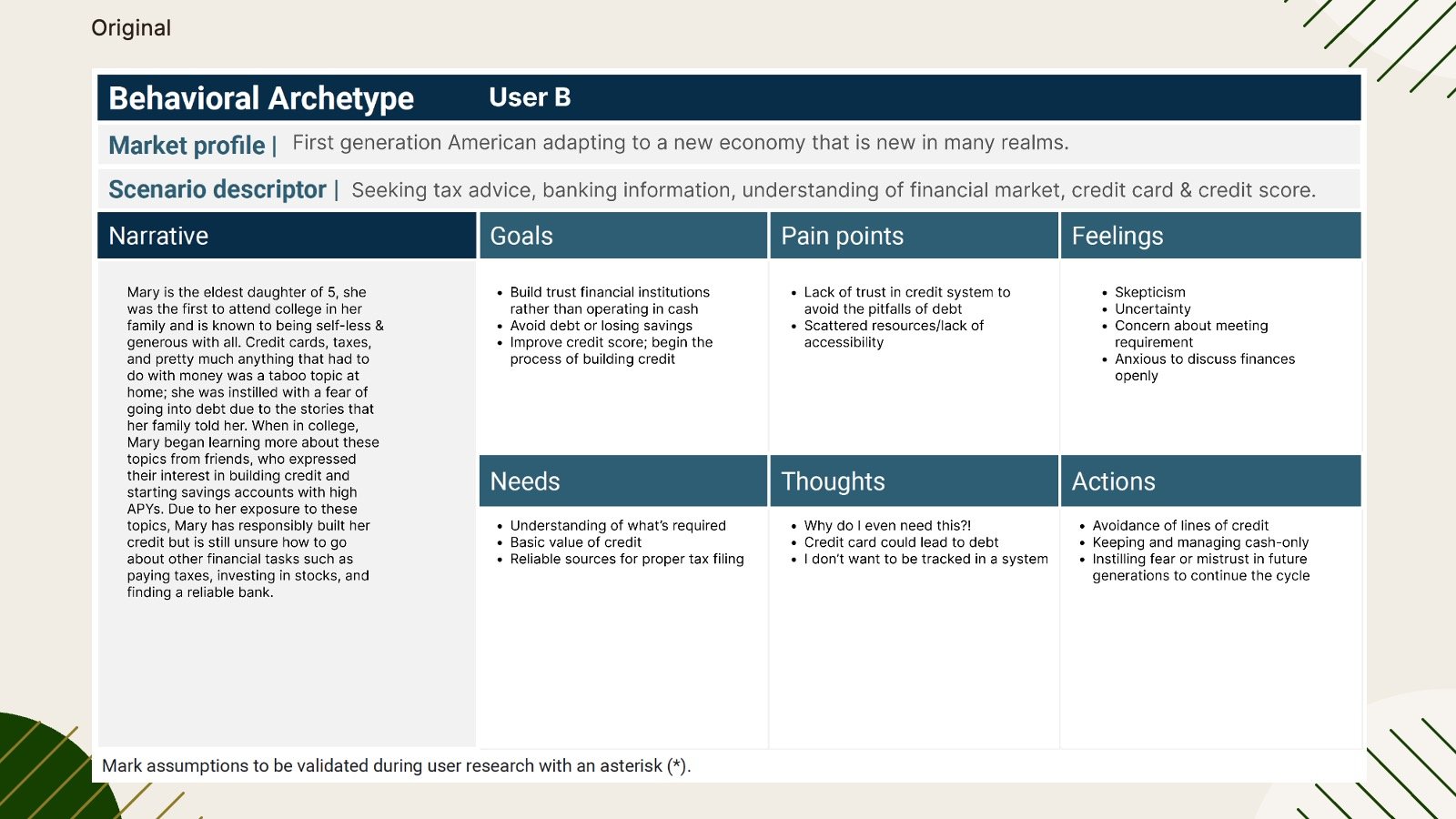

Original Behavioral Archetype

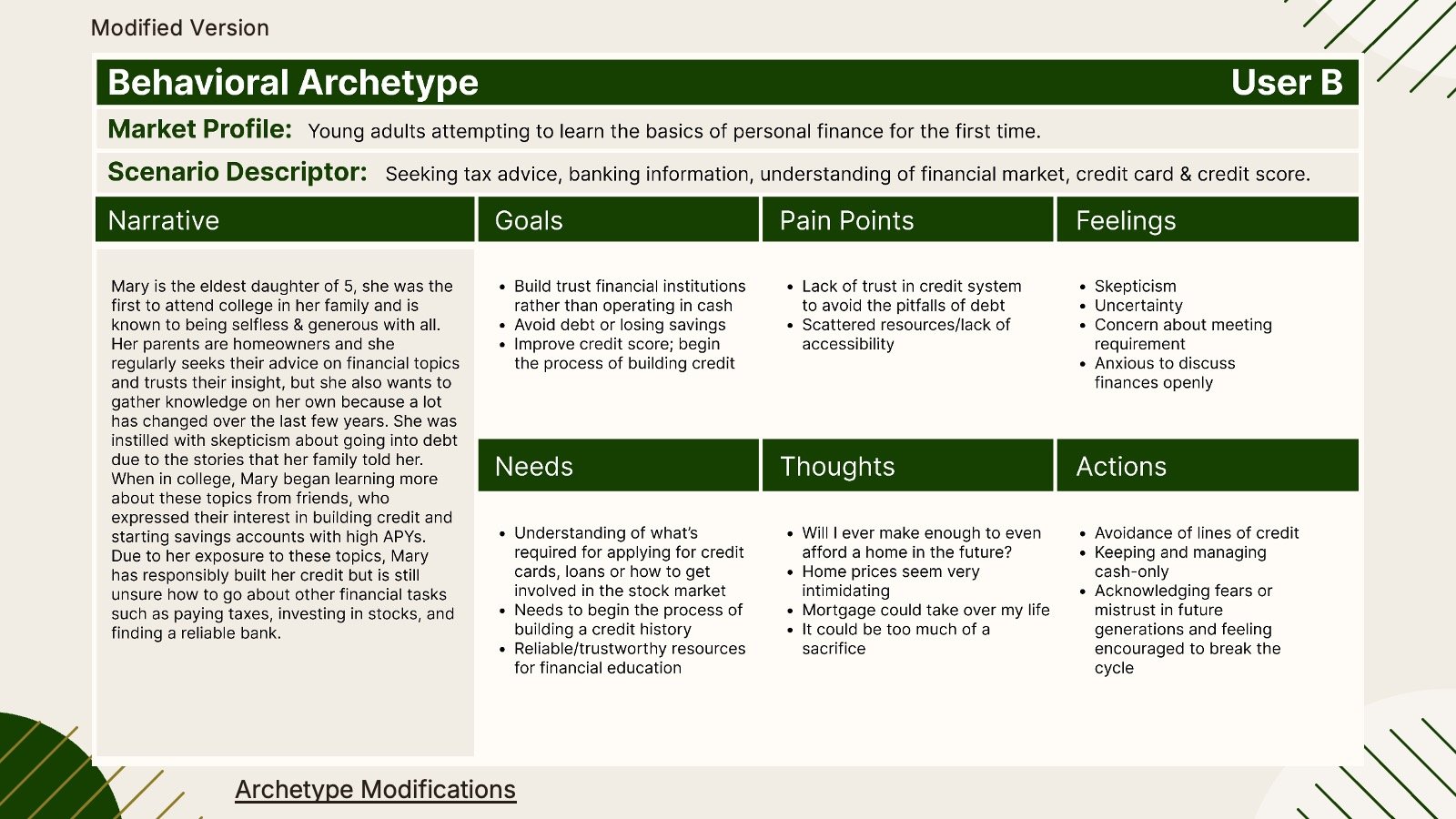

Modified Version Behavioral Archetype

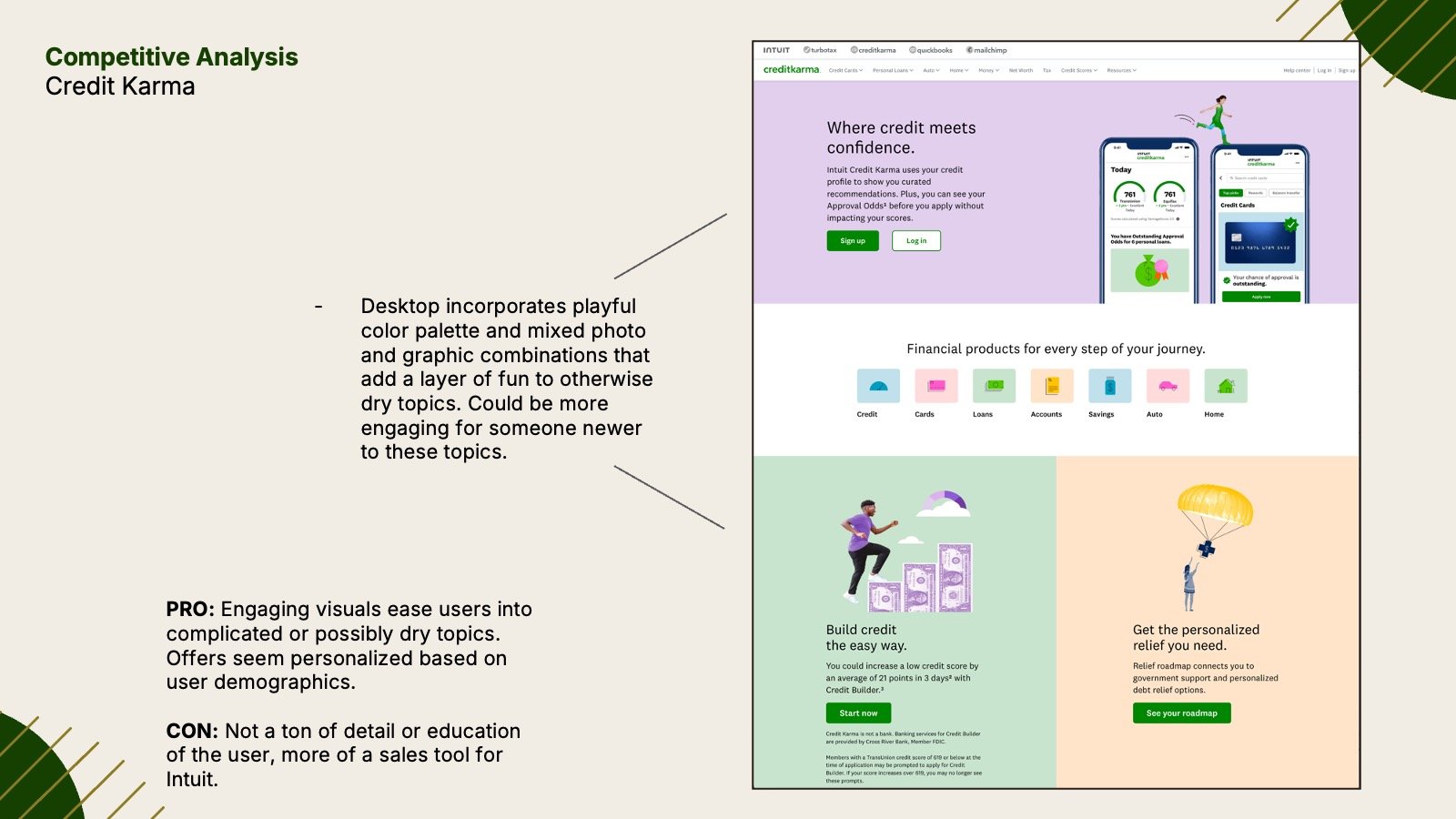

-

There is an inadequate understanding of basic home economics, including topics like responsible credit usage, the impacts of long-term debt, paying taxes, and retirement planning among a large portion of the population. Home Economics is rarely taught in schools to address this significant problem with serious consequences. Many people fall quickly into insurmountable credit card debt, file for bankruptcy at an early age or put their futures at risk simply as a result of understanding the basics of home economics. The research problem could be broken down into several key areas: Lack of Financial Education, Credit Card Misuse, Debt Management, Wealth Management and Applying for a Home Loan.

-

Tackle struggles around lack of financial resources and education.

Understand what resources users require for specific long term financial decisions.

Understand which specific points of financial processes are causing pain to users.

-

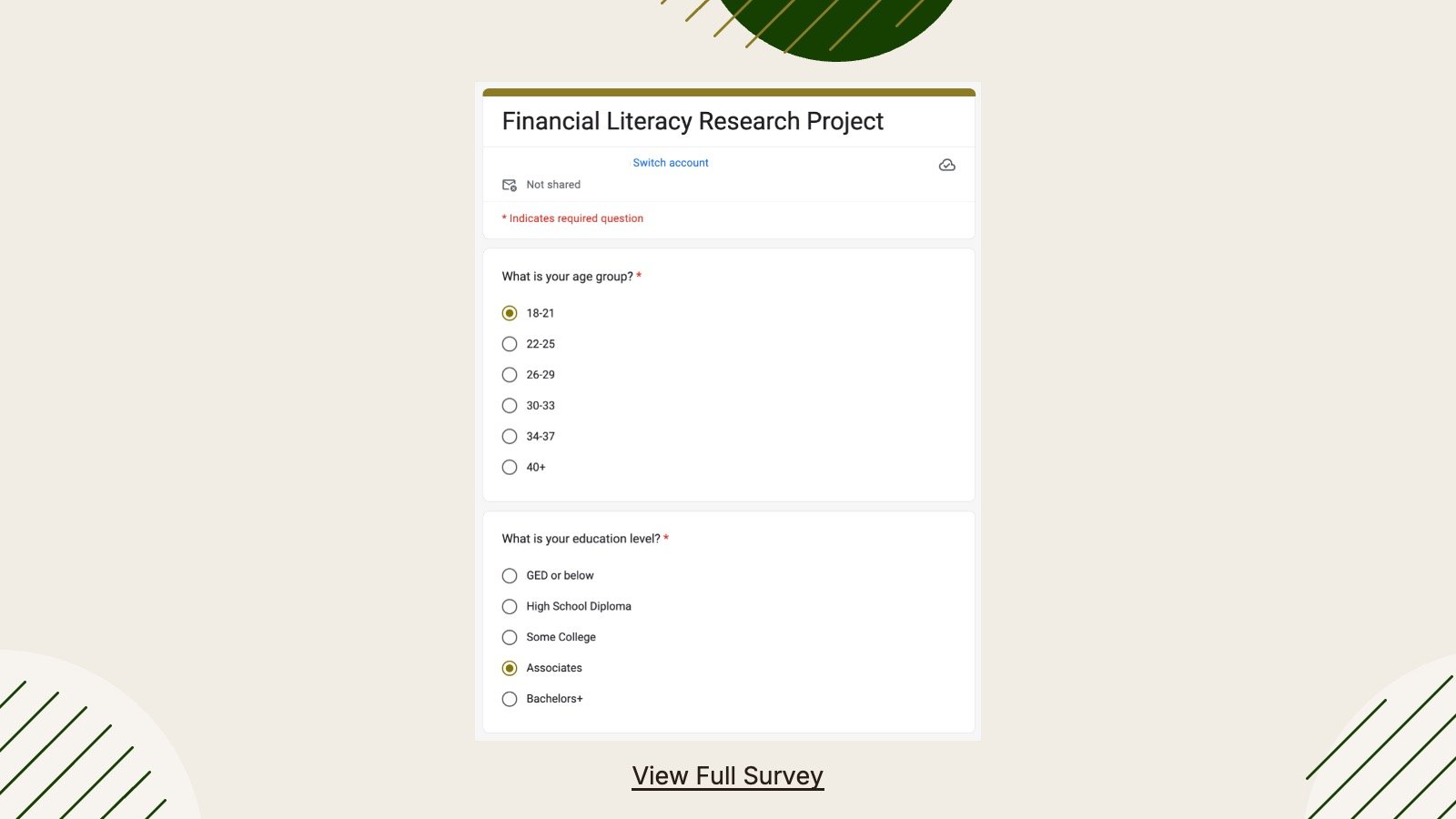

Through the collection of qualitative & quantitative data we attempted to further understand the pain points of individuals experiencing uncertainty and skepticism in regards to financial decision making. We conducted a total of 8 user interviews, users were privately messaged by researchers. We also collected data from a survey that provides further details on user behaviors and struggles surrounding financial literacy.

-

We are targeting a sample size of 4 participants total, two participants would identify as First-gen individuals navigating.

User A - Adults in their 40s considering buying a home.

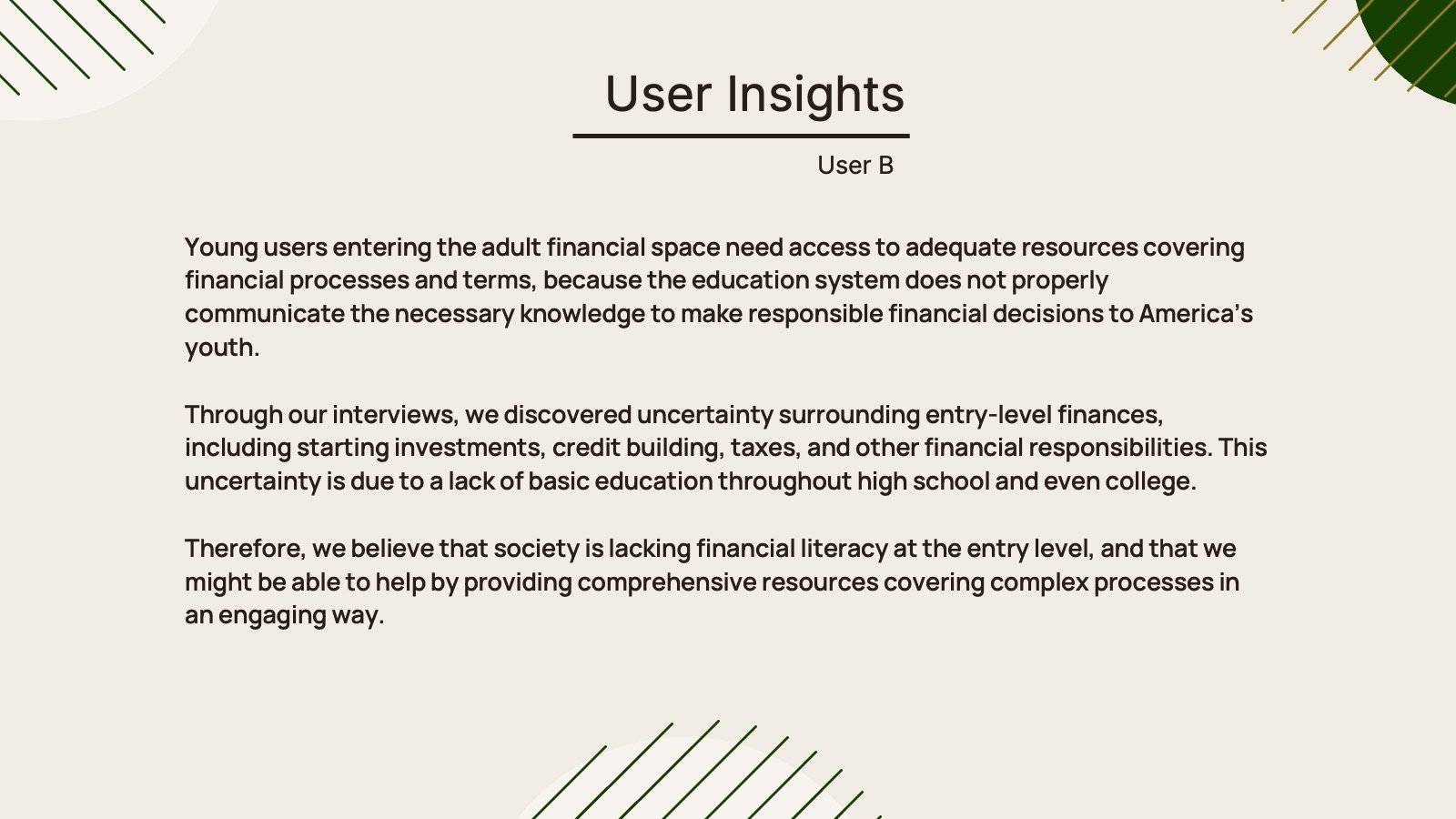

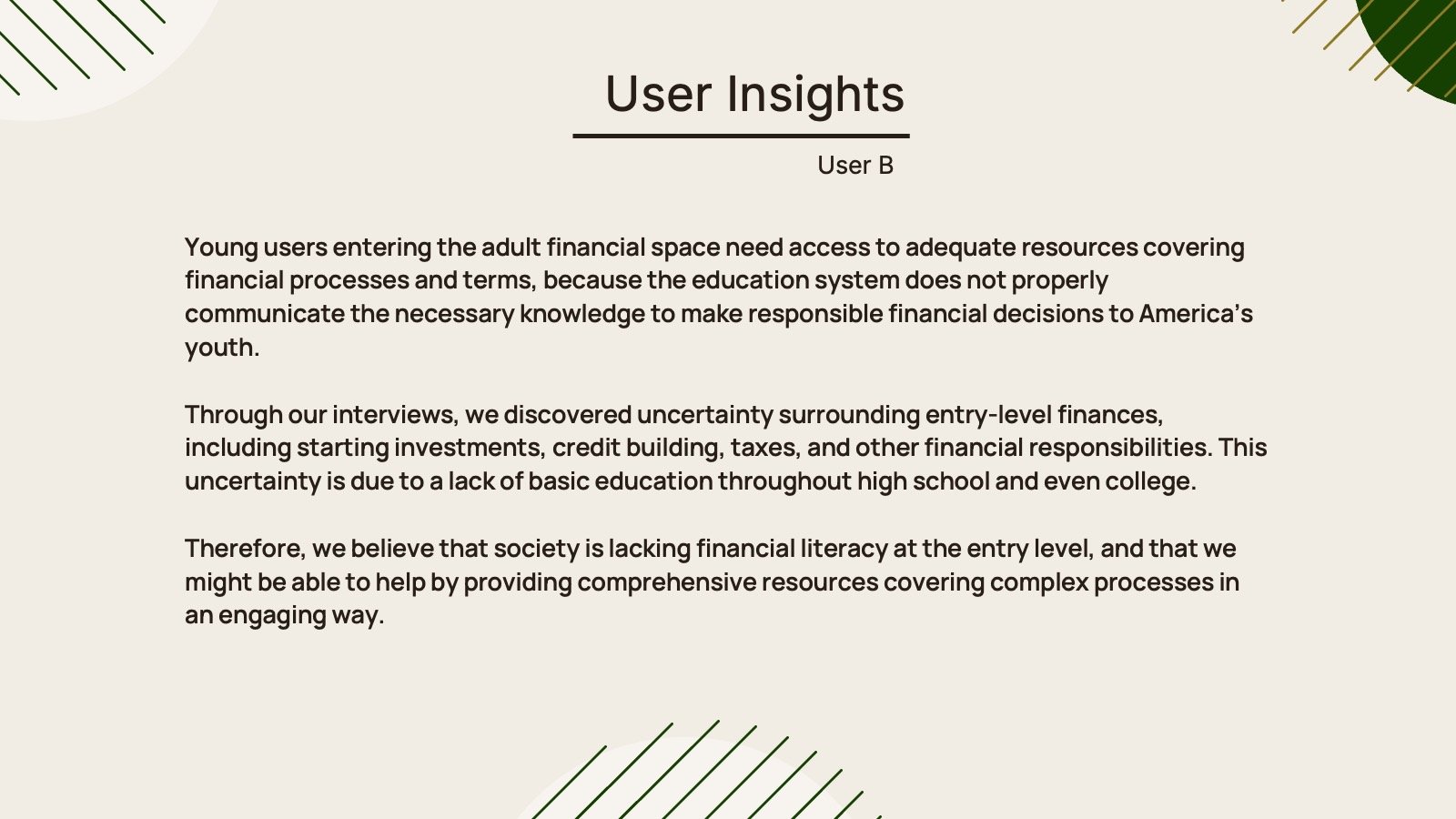

User B - 18-24 year olds who were not given access to home economics.

But are searching for resources on financial literacy (give rationale on the age groups - entering the ‘real world,’ gaining responsibility, new to taxes, student loans, investing, buying a car, etc.) description

INTERVIEW NOTES

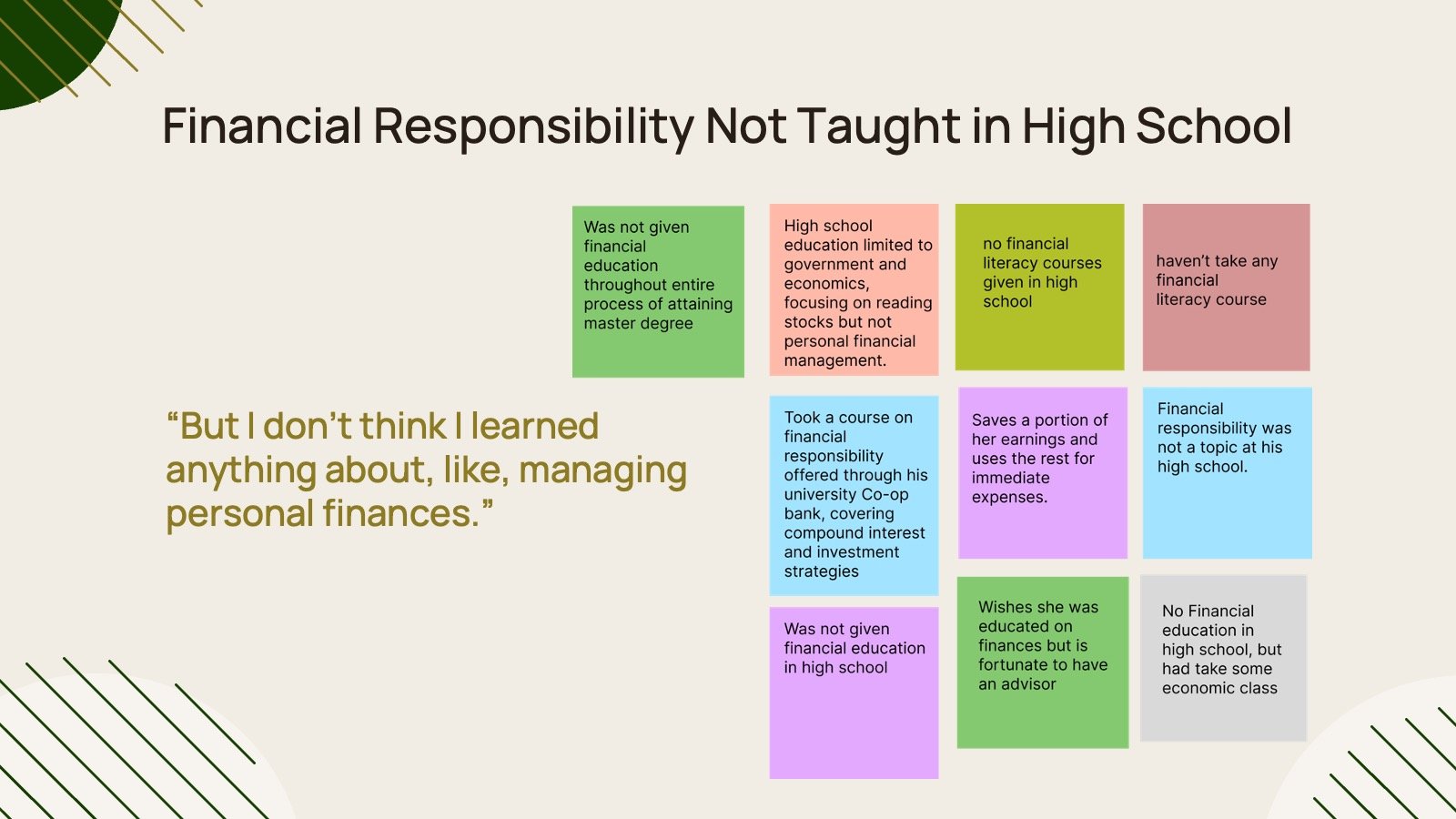

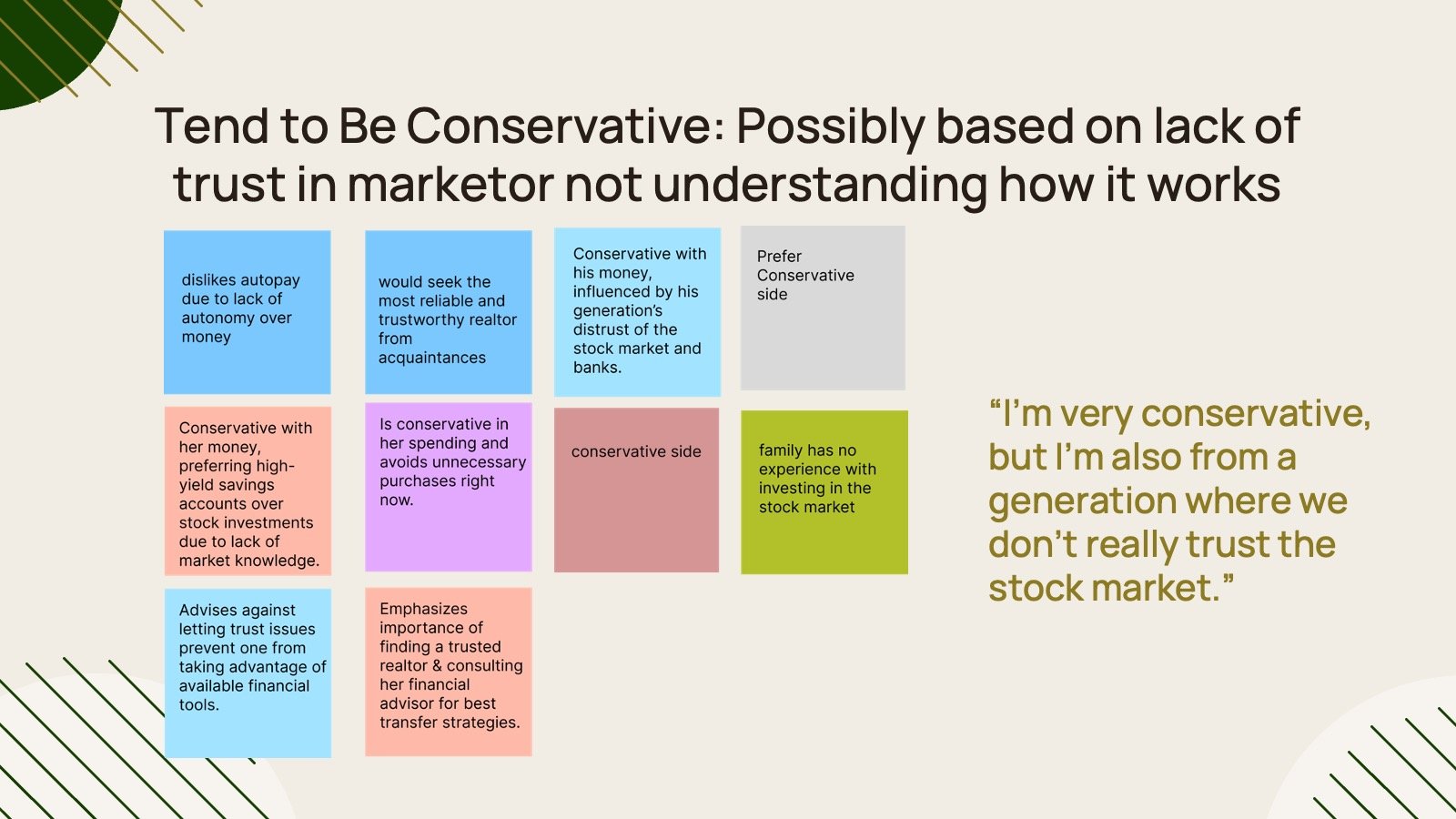

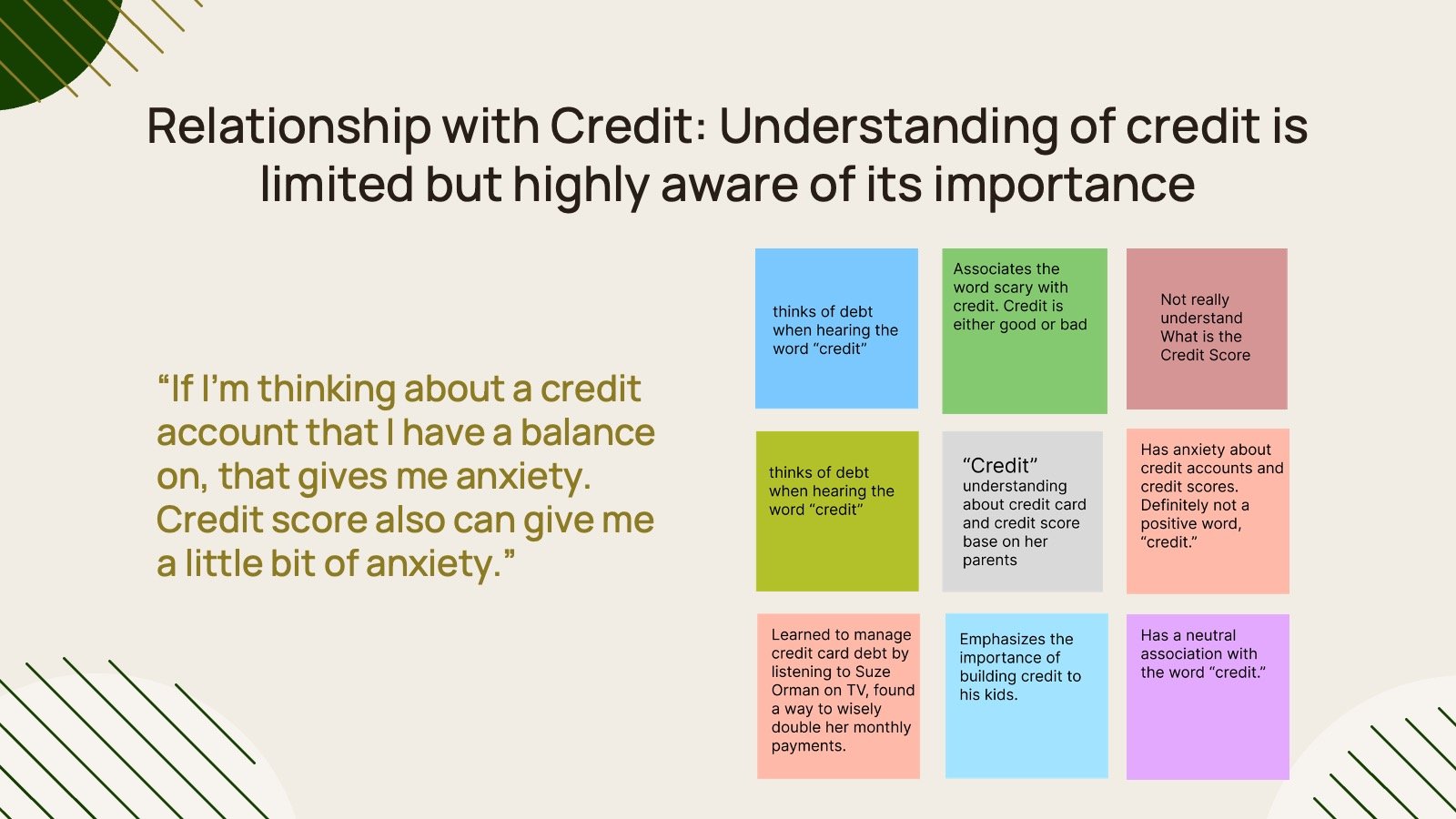

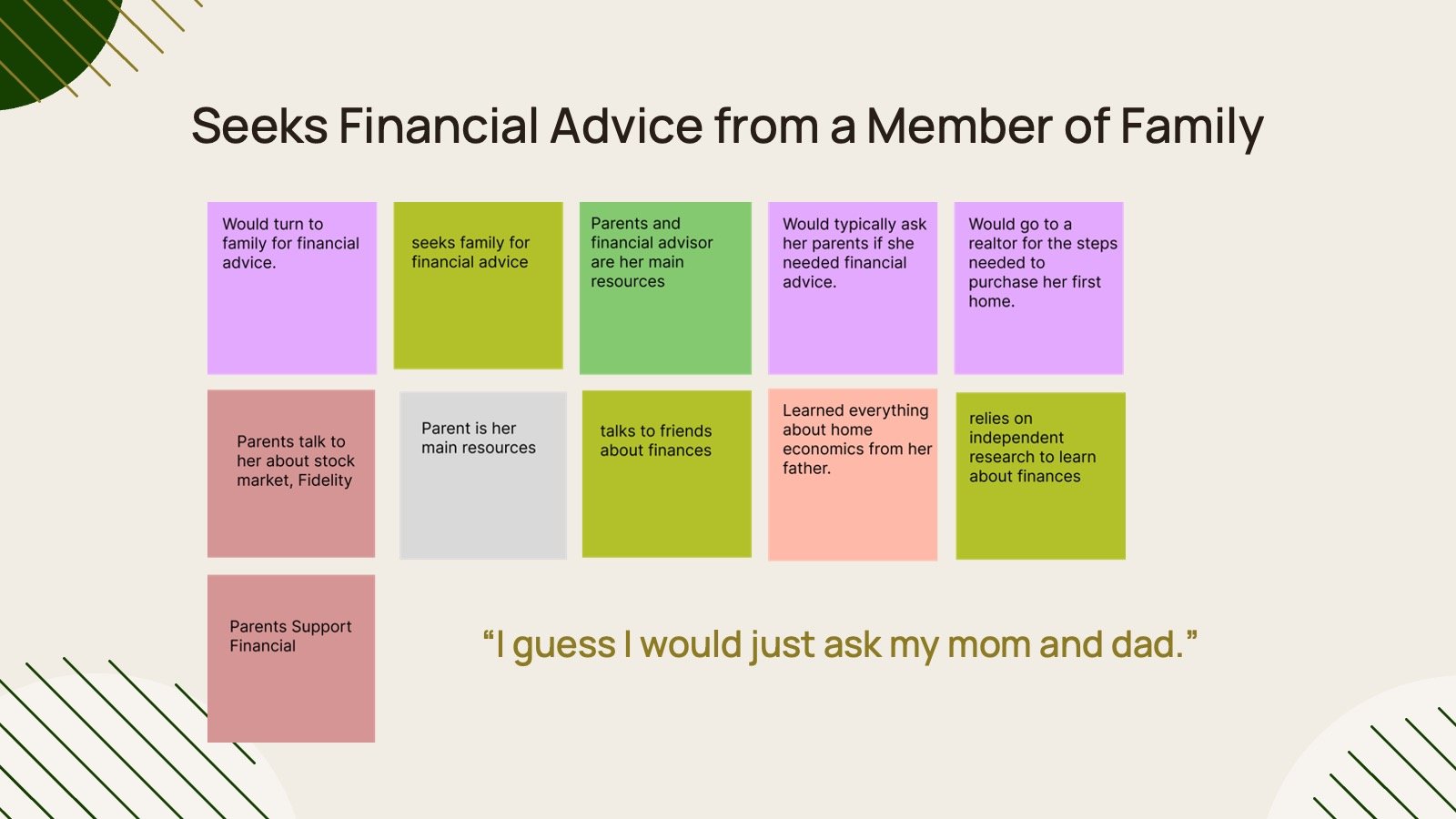

Savana is a 24 year old woman from Oak View, CA. She is currently finishing her masters in occupational therapy. She is appreciative of her parents support and is taking advantage of the freedom to grow her credit and save up money for large future purchases.

Amy is a working professional living in Austin, TX. She feels anxiety about credit and prefers conservative investments. Amy is saving for her daughter's education and future home ownership. She emphasizes the need for financial education and local resources to avoid pitfalls.

Terry received no high school education on personal finance and primarily relies on the internet, school, parents, and a high school counselor for financial knowledge. They manage finances with one checking account and recently opened a credit card to grow their credit. The interviewee associates credit with debt but acknowledges its importance.. Buying a home is seen as a significant financial commitment they are not yet ready for, citing high costs and limited income as potential barriers.

Alyssa, a 21 years old participant, shares that her high school did not provide much financial education but did offer economics classes; which proved unhelpful. She gets most of her financial advice from her parents, TikTok and Instagram. Alyssa knows the basics about credit information, but not much about credit scores. She is conservative with her money, using a savings account and Google Sheets to record her finances. She is interested in the stock market because some of her friends are investing in it. Alyssa wants to buy a small apartment in the future but doesn’t know how to start; she may ask her parents for support.

DISSEMINATION

The survey was directly distributed by researchers to specific participants who met the user criteria in addition to being posted on social media platforms such as Snapchat and Instagram. The survey posts were designed to explicitly state the user criteria for participants in order to receive relevant data.

Describe your relationship with your finances in one word.

30 responses

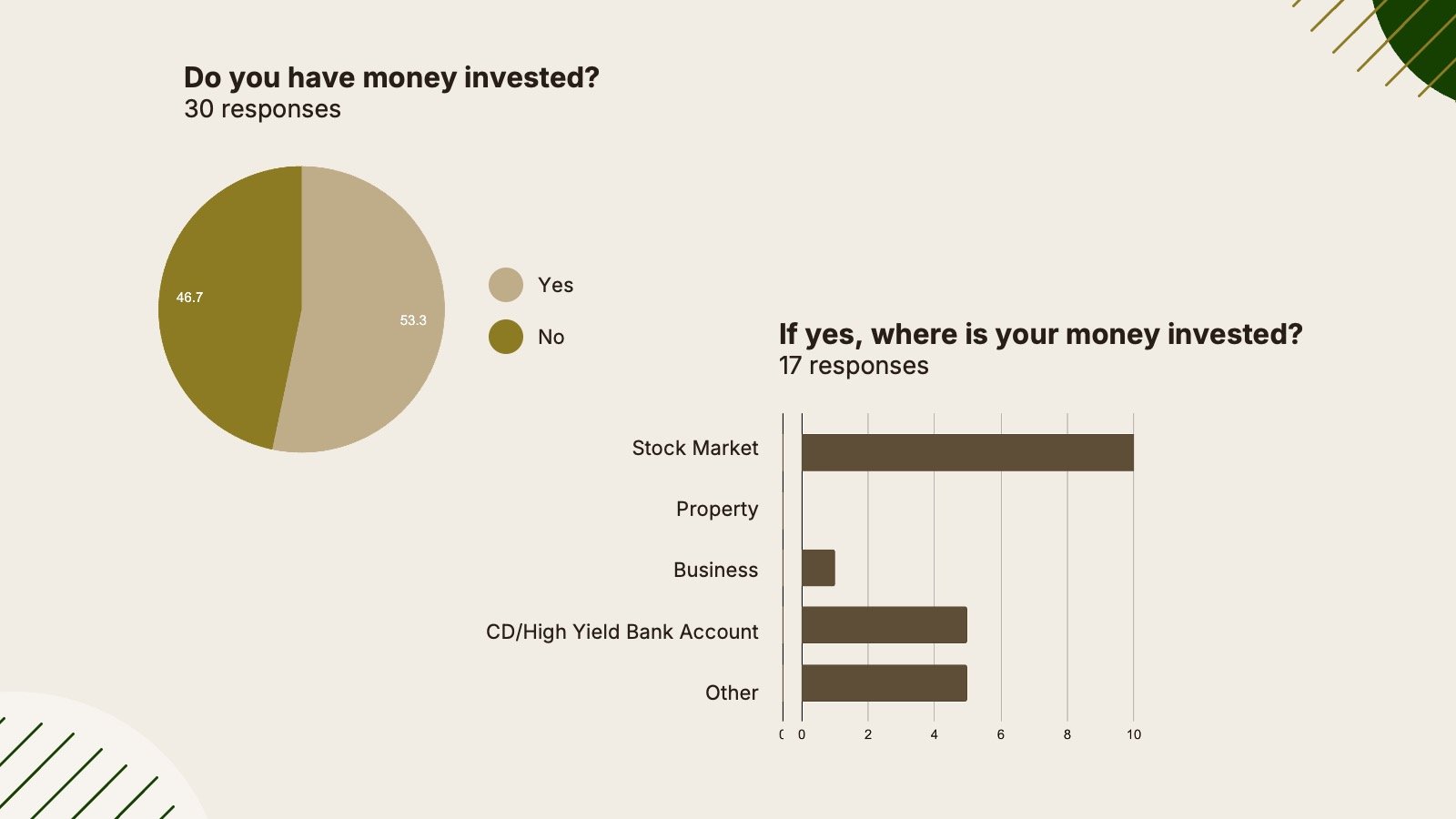

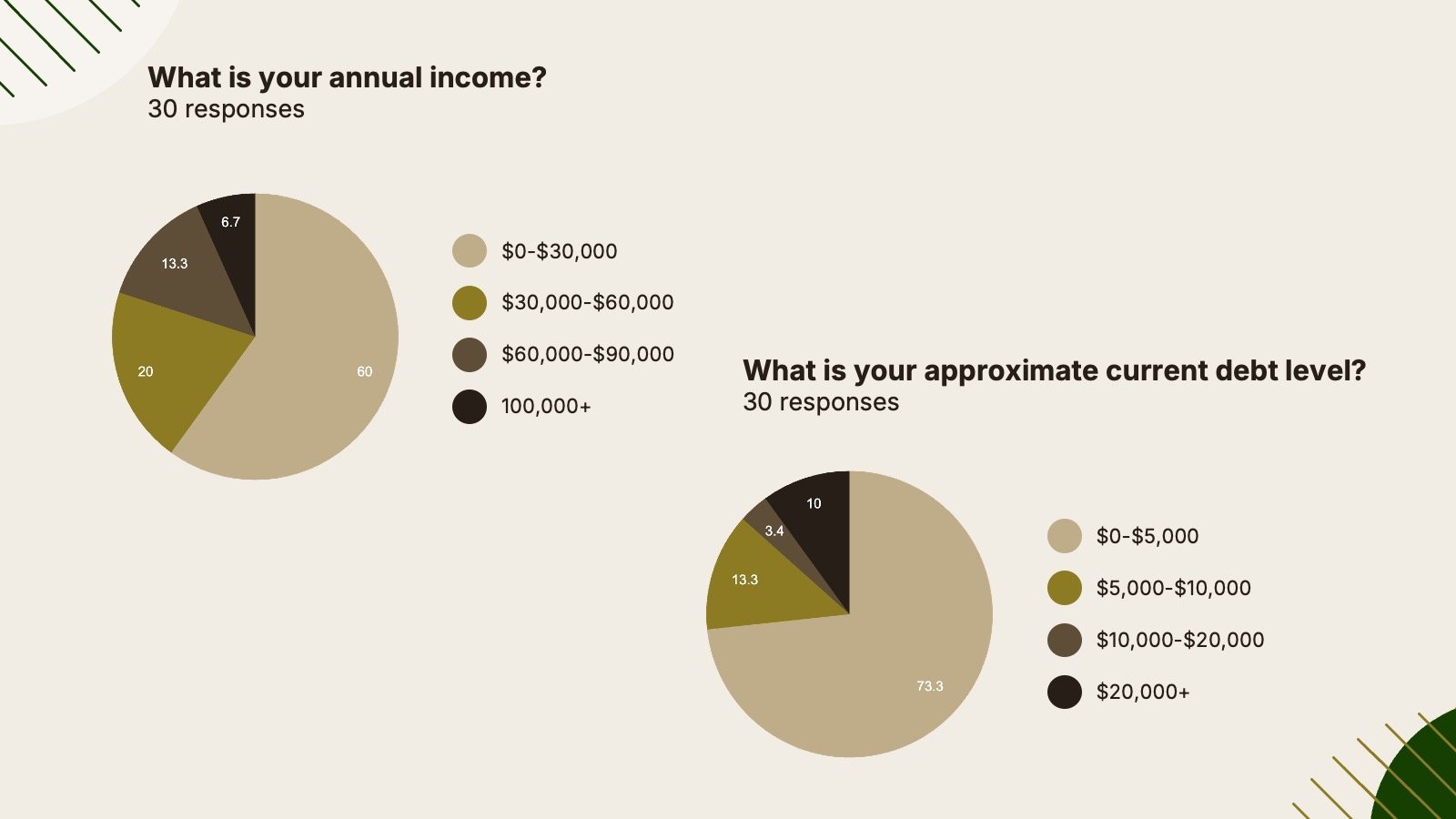

KEY FINDINGS

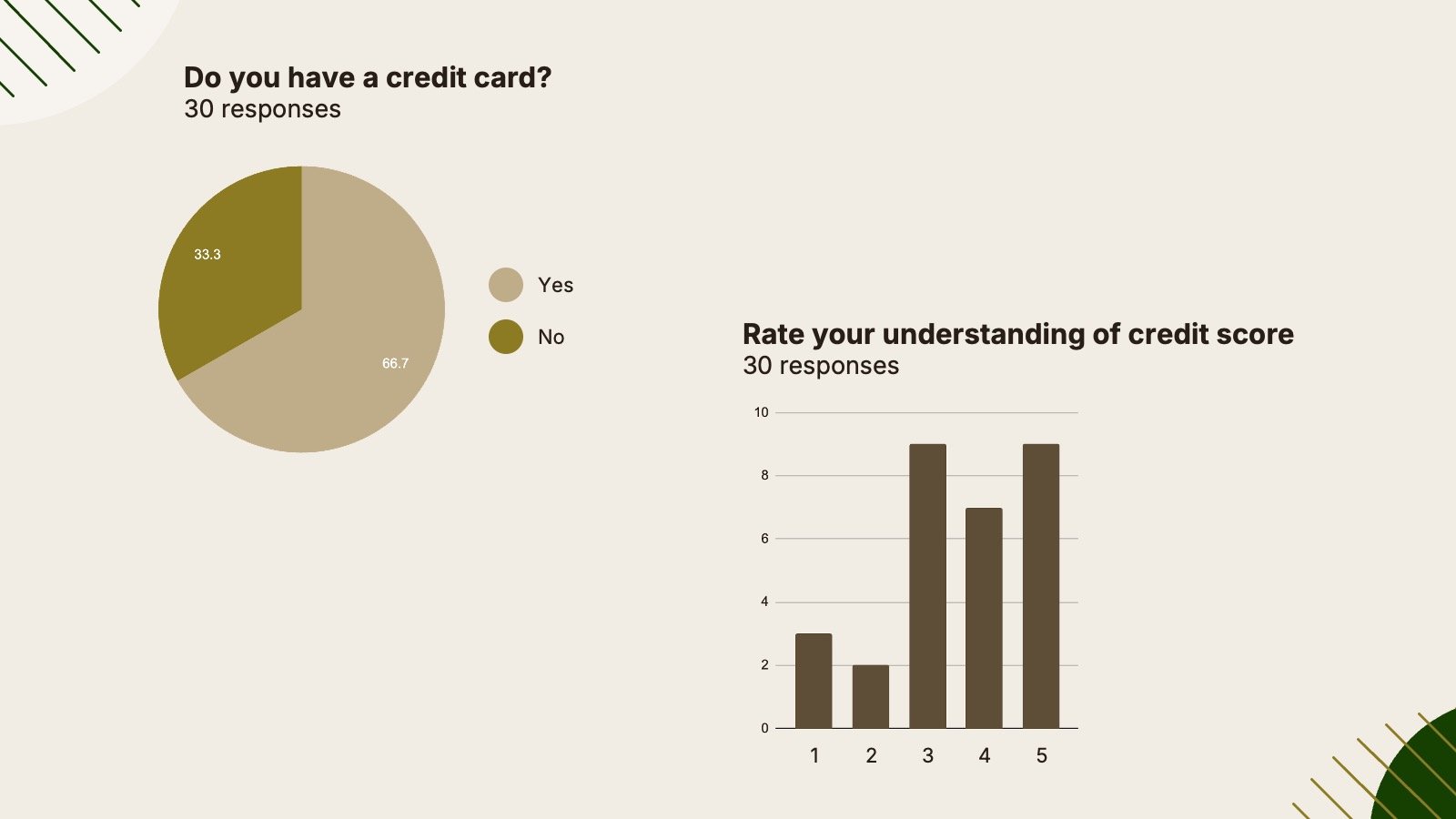

66.7% of participants have a credit card but only 30% feel they have a true understanding of credit score.

• which can be greatly impacted through irresponsible credit card usage.

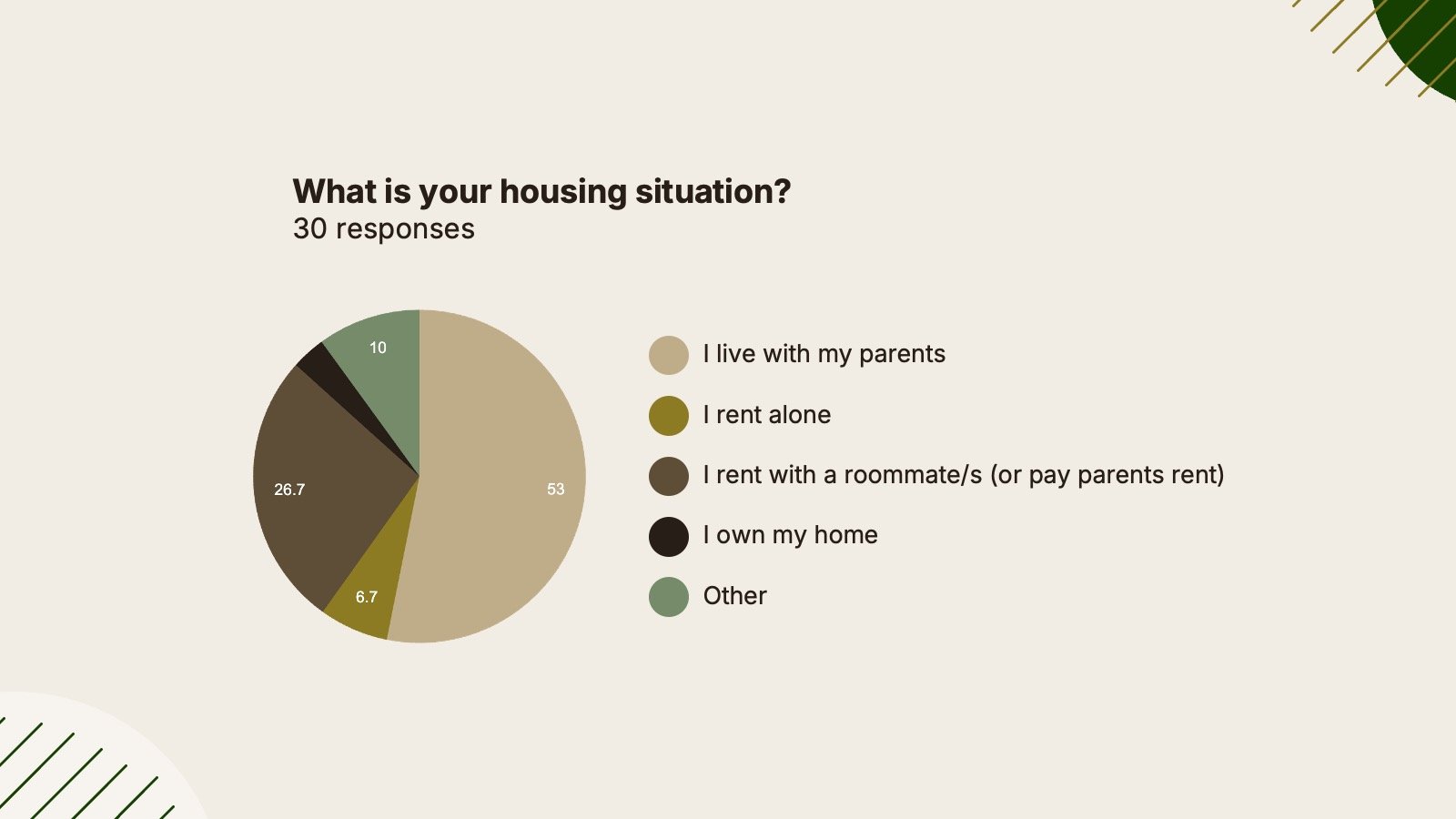

53% of participants live with their parents. From this we can assume that these participants will seek out financial resources when planning to move out.

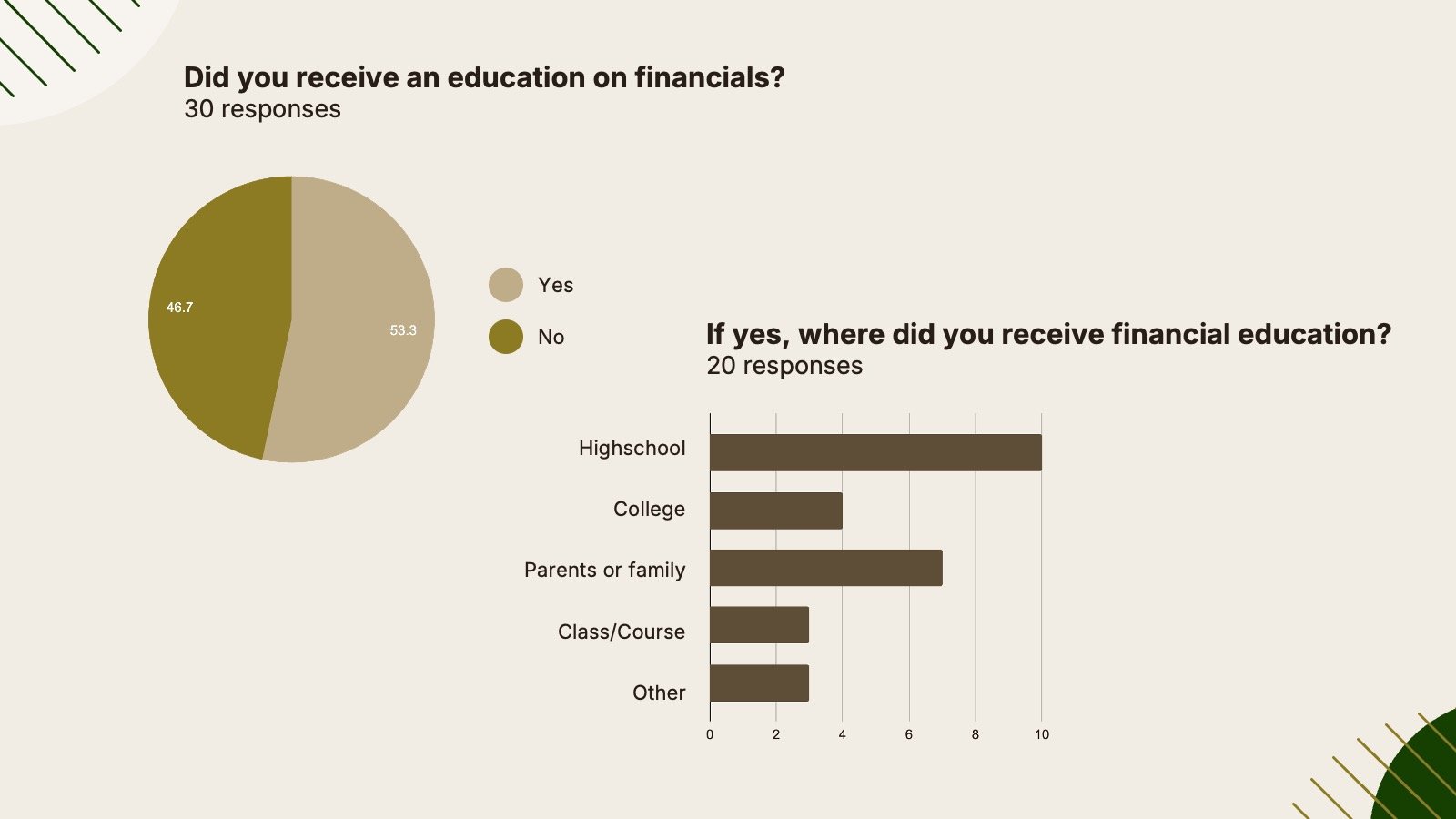

53% of participants feel they have received an education on finances. Of those 53.3%, half believe they received financial education in high school.

This is significant because our interviewees all shared not receiving an applicable education on financials in high school.

38% of participants aged 18-21 rate their understanding of credit score below 60% or below; yet, 52% have a credit card.

LIMITATIONS AND CHALLENGES

Interview Process: we experienced a lack of access to older generations that would be willing to participate in this interview

Survey Questions:

“Did you receive an education on financials?”

“If yes, where did you receive financial education?”

Education level or education quality was not asked, therefore we do not know what participants are qualifying as a “high school financial education”

Vague questions

Should have followed up with what subjects of finances were taught

Believed these answers are skewed and inaccurate

Adds to the point that Americans tend to believe they know more about finances than they actually do

Research Conclusions

Populations aged 18-21 are struggling with financial literacy due to a lack of prioritization in the American education system. When entering the financial space, individuals need resources for learning, retaining, and applying financial learnings.

Participants who are over the age of 21 reflected back on their education and shared that much of their knowledge has come from advisors, parents, and personal research.

Being financially literate is crucial in building credit, buying a home, loan approvals and general wellbeing.

Frustrations surrounding lack of resources and understanding regarding personal finances have encouraged our team to find an accessible and applicable solution.

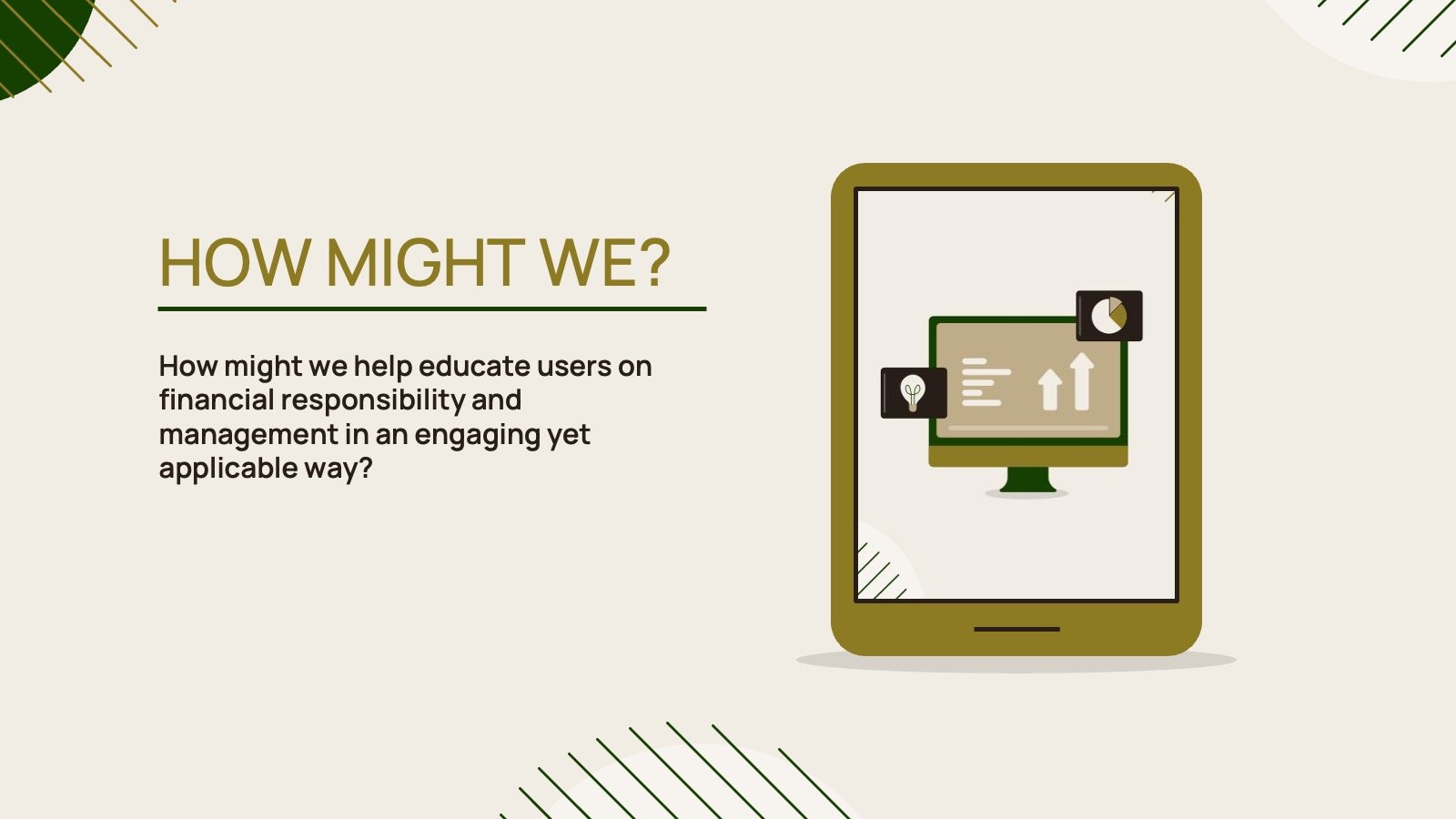

Problem Statement

We believe the general population of non-homeowners are under-educated and unaware of the weighted consequences related to financial responsibility and literacy. Therefore, access to educational materials will help build confidence and applicable knowledge when navigating the complex world of personal finance.

Recommendation and Next Steps

Regardless of what stage of life one is in, all participants feel they would benefit from financial education. Based on this we would recommend an accessible educational app that uses engaging and fun activities to instill confidence in users who strive to gain financial control

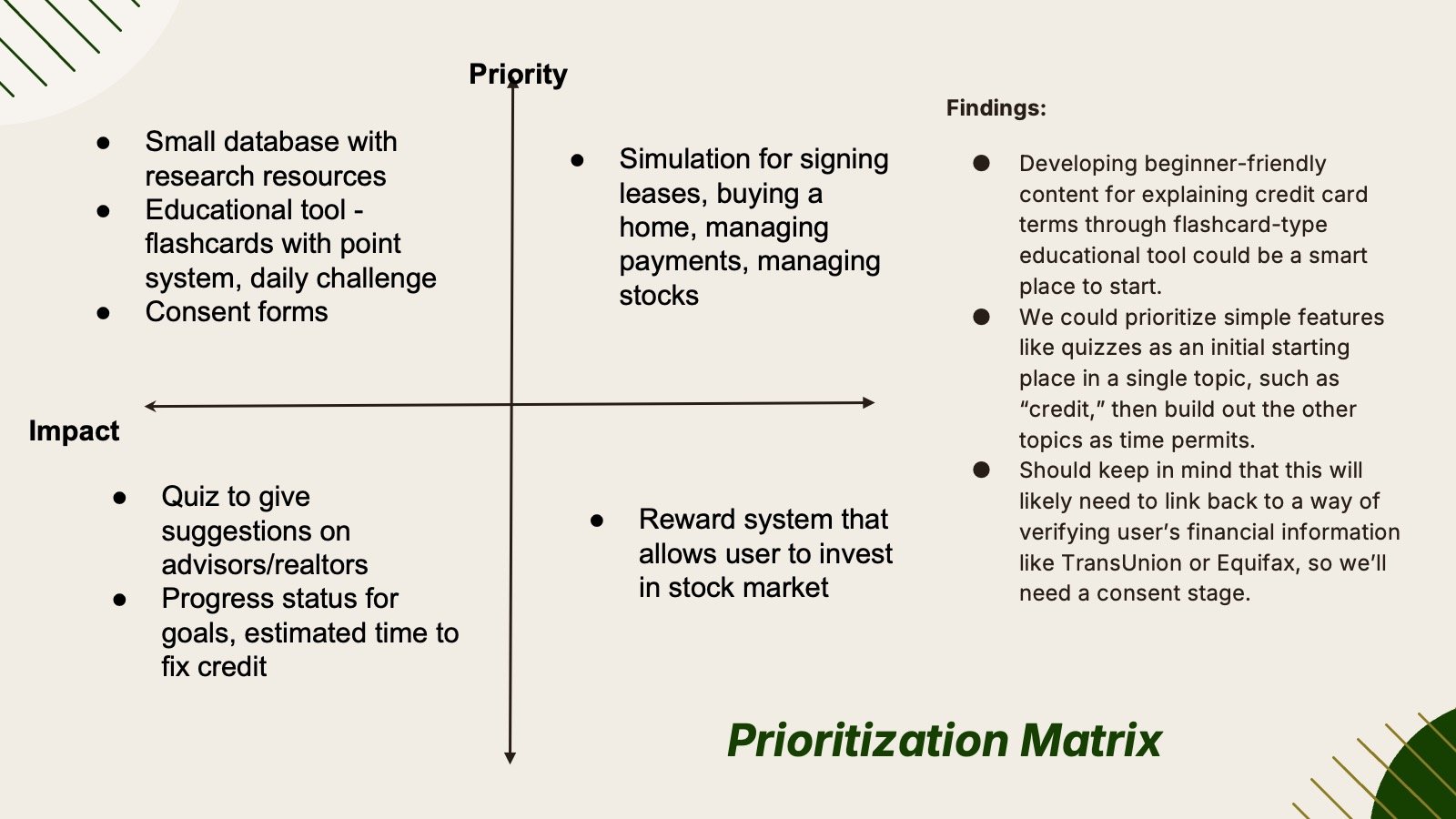

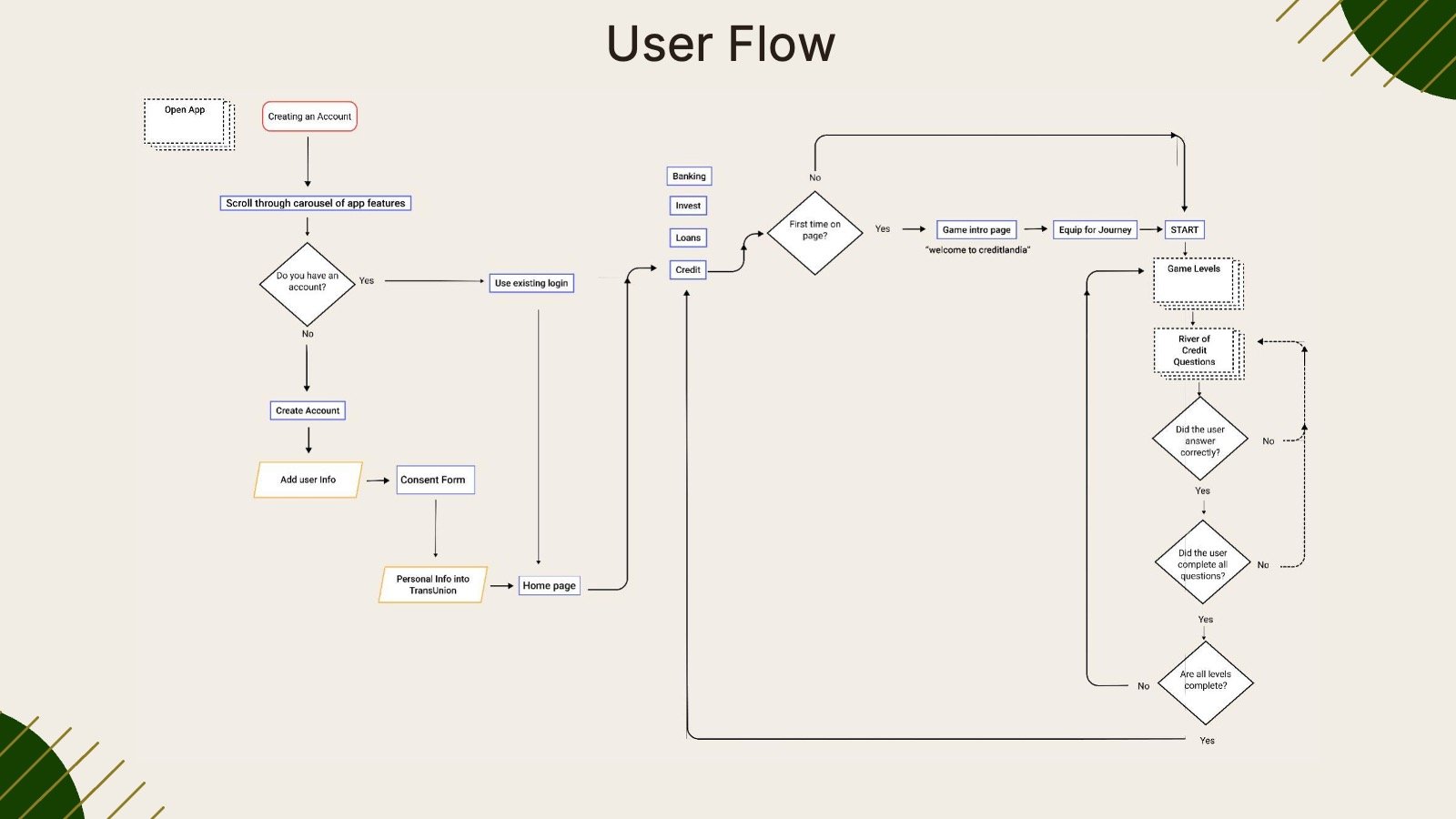

Ideation Process

Wireframe Prototype

Interactive Prototype

Conduct Usability Tests

Key points included:

●The need to make type and tagline more readable

●Suggesting a more playful name

●Ensuring consistency in the characters’ appearance

●Testers found the app engaging but suggested keeping the color palette cohesive and making the game-like elements more intuitive.

They appreciated the gamification aspect and believed it could motivate users to learn about their credit scores and financial management.

Conduct Usability Tests

Key points included:

Users navigate more intuitively than we had designed for

on the search results page when users clicked directly on the search result rather than utilizing the ‘learn more’ button

Next Steps

Descriptions include hyperlinks to external resources, our app would serve as the bridge between the user and the source.

Animated game levels that are engaging and interactive

Further game categories and levels